Perpetual futures funding rate: how it actually works

A perpetual futures funding rate is a recurring payment between LONG and SHORT legs that keeps a contract without an expiry close to its reference price. Positive funding usually means longs pay shorts; negative funding reverses the flow. The displayed rate belongs to one interval, so its sign, interval and persistence matter more than an annualized headline.

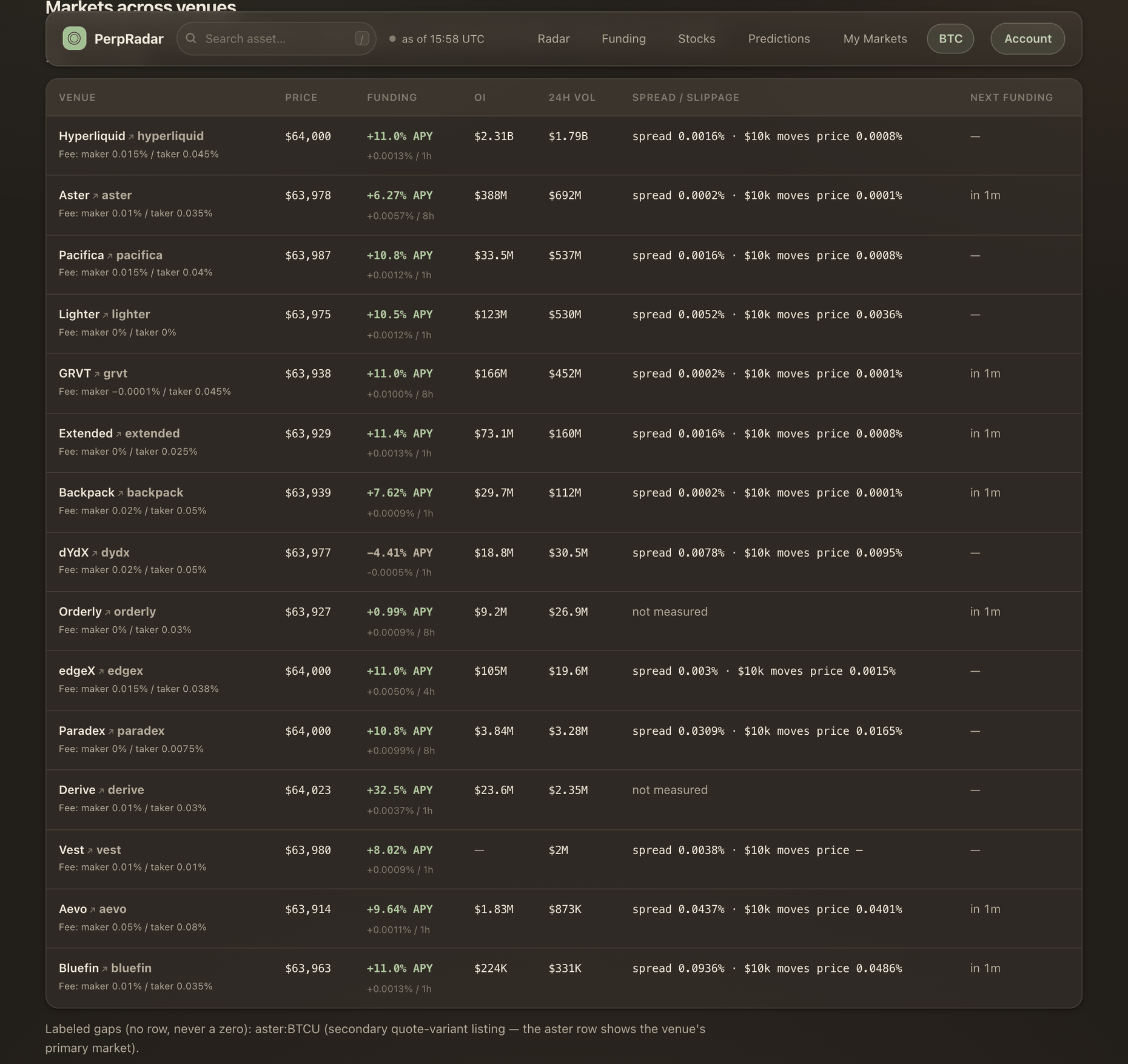

Examples use PerpRadar measurements captured July 10, 2026, 15:58–16:08 UTC. They are dated observations, not current rates.

Why perpetual futures need a funding rate

A dated futures contract eventually settles, which pulls its price toward the underlying market. A perpetual contract has no expiry. Without another anchor, its price could remain above or below spot for much longer.

The funding rate supplies that anchor through recurring transfers between the two sides of the perp market. When the perp trades above its reference price, the rate usually turns positive and LONG legs pay SHORT legs. When it trades below the reference, the rate can turn negative and SHORT legs pay LONG legs. The venue does not need to predict direction; it makes the visible price gap costly to maintain.

Who pays the perpetual futures funding rate?

The sign answers the payment direction, not whether a market is attractive:

- Positive funding → LONG legs pay; SHORT legs receive.

- Negative funding → SHORT legs pay; LONG legs receive.

The cash amount is normally the funding rate multiplied by the leg's notional value. A +0.0013% hourly rate on $10,000 is about $0.13 for that interval. The next interval can use a different rate, so one payment should not be treated as a stable daily or yearly income stream.

Why the interval matters as much as the rate

Venues publish rates on different clocks. In the BTC venue comparison captured on July 10, Hyperliquid displayed +0.0013% per 1 hour, edgeX +0.0050% per 4 hours, and GRVT +0.0100% per 8 hours. The raw 8-hour number looked larger, but its hourly pace was lower than Hyperliquid's.

Put the three prints on the same $10,000 notional and the comparison becomes concrete:

| BTC venue | Raw print | Interval payment | 24h payment | Simple annualized |

|---|---|---|---|---|

| Hyperliquid | +0.0013% / 1h | $0.13 each hour | $3.12 | 11.39% |

| edgeX | +0.0050% / 4h | $0.50 every 4h | $3.00 | 10.95% |

| GRVT | +0.0100% / 8h | $1.00 every 8h | $3.00 | 10.95% |

The largest raw percentage does not produce the largest daily payment. First normalize the clock: hourly equivalent = raw print ÷ interval hours. Then compare direction, dollars and persistence.

How a funding rate becomes an annualized number

The three useful calculations are:

Payment per interval = notional × raw rate

Simple annualized rate = hourly equivalent × 24 × 365

An hourly 0.0013% print becomes 11.39% annualized and $3.12 per day on $10,000. This is an APR-like projection, not a true compounded APY, and it assumes the print remains unchanged for 8,760 hours.

That assumption is the weak link. On the same measurement window, the leading HYPE setup on the funding table moved from 222% to 195% annualized in seven minutes. The arithmetic stayed correct; the input changed.

Current, predicted and settled funding are different

A funding number is incomplete without its state:

- Current — the latest rate exposed for the active interval.

- Predicted — an estimate of the rate expected at the next settlement; it can change before then.

- Settled — a historical rate that produced an actual transfer.

Use settled history to measure persistence. A predicted print is useful for observing the next interval, but it should never be mixed into a historical series as though the payment already happened.

How to read a funding row in 20 seconds

- Read the sign and identify which side pays.

- Confirm the funding interval.

- Check whether the number is current, predicted or settled.

- Convert it into dollars at the intended notional.

- Read the timestamp and freshness state.

- Compare the 24-hour range and sign flips.

- Put spread, fees and measured book depth beside the expected transfers.

The rate alone does not tell you whether it will persist or whether costs consume the transfers. Compare the calm BTC page with the thinner HYPE page: the same rate vocabulary sits on very different market structure.

Source and measurement scope

The examples above are historical PerpRadar observations captured on July 10, 2026. Hyperliquid's official perpetuals API documents current funding, open interest and funding history. PerpRadar applies the same discipline to every venue adapter: retain the raw print, verify its interval and label unavailable fields as gaps.

FAQ

- What is a perpetual futures funding rate?

- It is a recurring transfer between long and short legs that helps keep a perpetual contract near its reference price. The venue calculates the rate for a defined interval; the sign determines which side pays.

- Who receives a positive funding rate?

- SHORT legs normally receive positive funding from LONG legs. When funding is negative, the direction reverses and LONG legs receive from SHORT legs.

- How do you compare 1-hour and 8-hour funding rates?

- Normalize both to one period. Divide an 8-hour print by eight for an hourly equivalent, then compare it with the 1-hour print. Do not compare the two raw percentages directly.

- Is an annualized funding rate guaranteed for a year?

- No. It projects the latest normalized print across a year. The rate can change at the next interval; one measured HYPE setup moved from 222% to 195% annualized in seven minutes.