Negative funding rate meaning: who pays whom in perps

Negative funding rate meaning is simple: SHORT legs pay LONG legs for that funding interval. It usually appears when a perpetual trades below its reference price, making the crowded short side pay. The sign does not guarantee a price reversal or a lasting yield; interval, persistence, liquidity and venue rules determine what the print actually represents.

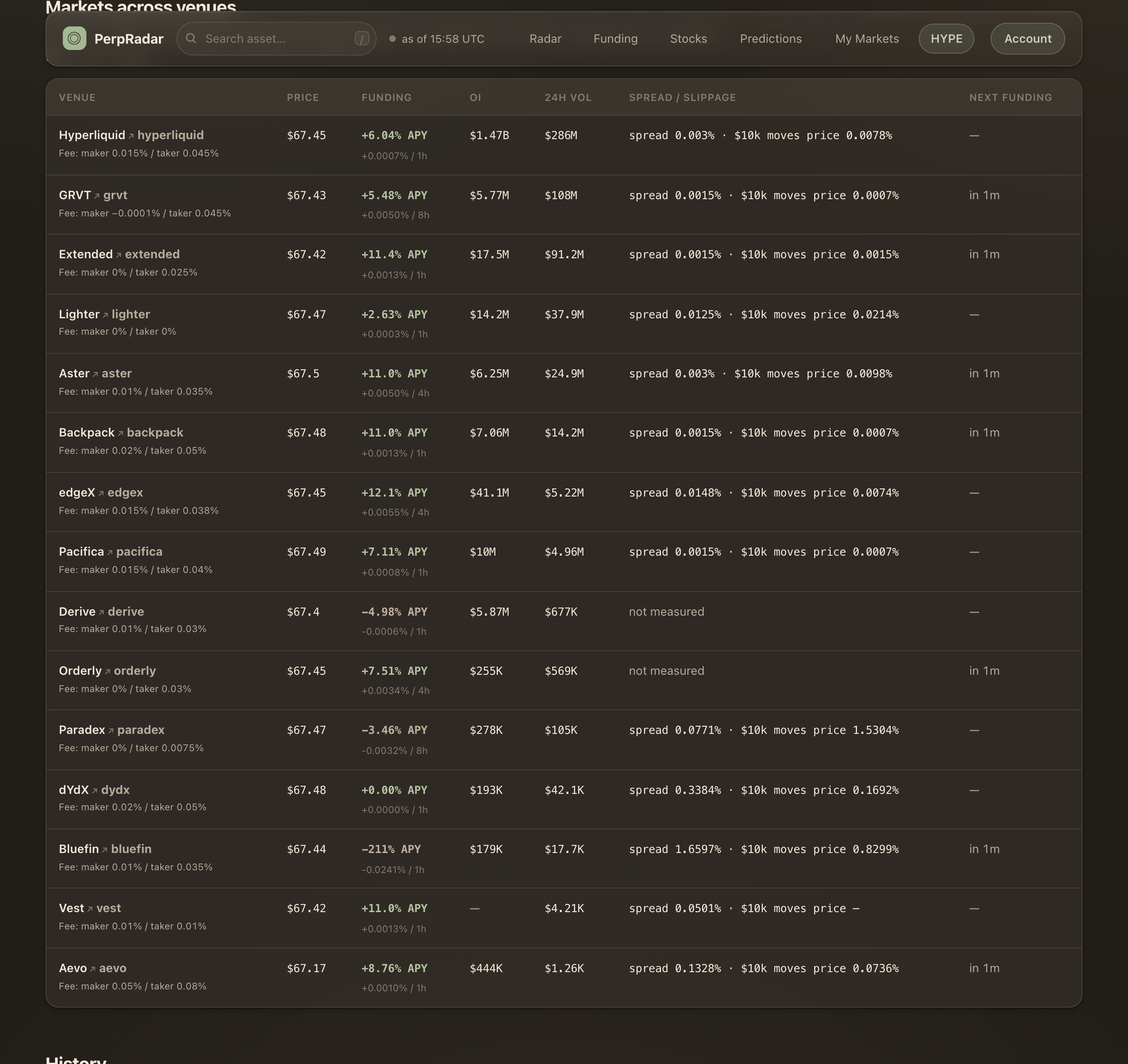

The example below was measured on July 10, 2026, 15:58–16:05 UTC. It is historical evidence, not a current rate.

Who pays when funding is negative?

Negative funding reverses the more familiar positive flow:

- Negative funding → SHORT legs pay; LONG legs receive.

- Positive funding → LONG legs pay; SHORT legs receive.

The sign belongs to a specific venue, market and interval. A −0.0241% hourly print means the receiving LONG leg accrues 0.0241% of its notional for that interval under that venue's rules. It does not mean the same rate will remain negative at the next print.

Why does a funding rate turn negative?

A negative rate usually appears when the perpetual trades below its reference price. The payment makes the crowded SHORT side more expensive to hold and rewards the LONG side, creating an incentive for the perp price to move back toward the reference.

That can reflect bearish crowding, a temporary price dislocation or venue-specific market structure. The rate is evidence about the current perp premium or discount; it is not a standalone forecast of the next price move.

A measured −0.0241% hourly HYPE print

On July 10, the HYPE venue page showed Bluefin at −0.0241% per hour, displayed as −211% annualized. The number was large, but the same market carried only $179K of open interest, $17.7K of daily volume and a 1.66% spread.

On the receiving Bluefin LONG leg alone, before including the second venue, $10,000 at −0.0241% produced $2.41 per hour, or $57.84 per day if the print held. Using the displayed 1.66% spread as a simplified round-trip cost proxy — half-spread on entry plus half-spread on exit — gives $166 before fees and additional slippage.

| Rate observation | Funding / hour | Funding / day | Break-even on $166 |

|---|---|---|---|

| −0.0241% at 15:58 UTC | $2.41 | $57.84 | 68.9h / 2.9 days |

| −0.0209% at 16:05 UTC | $2.09 | $50.16 | 79.4h / 3.3 days |

Seven minutes of rate movement extended the simplified recovery window by more than ten hours. The cross-venue setup at the top of the funding table also had a receiving Extended leg, but a combined calculation must include funding and round-trip cost on both venues rather than mixing a one-leg cost with a two-leg headline.

The break-even clock matters more than the annualized headline

Two-leg break-even hours = both-leg round-trip cost USD ÷ expected net funding USD per hour

If the −0.0241% print lasted only six hours, the receiving leg would collect $14.46. Against the $166 simplified spread proxy, $151.54 would still be unrecovered before fees and additional slippage.

That is where persistence becomes useful. Compare the required 68.9 same-sign hours with the observed sign-flip history. A projection that needs three stable days is weakly supported when the recent series changes direction repeatedly within one day.

Does negative funding mean the price will rise?

No. Negative funding can show that the perp is below its reference or that SHORT exposure is crowded, but crowding can persist. Price can continue lower while SHORT legs keep paying. Funding is a transfer mechanism, not a reversal timer.

To interpret it, add context: recent sign flips, perp premium, open interest, volume and book depth. A single negative print with thin liquidity is different from a small negative rate that persists across a deep market.

Five negative-funding situations that look similar but are not

| Observed state | What it can mean | What to check next |

|---|---|---|

| Negative on one venue | Local imbalance or venue-specific thin liquidity | Same asset across other venues |

| Negative across most venues | Broader perp discount or SHORT crowding | Premium, open interest and duration |

| Negative and stable | Same payment direction has persisted | Break-even versus same-sign hours |

| Negative with many flips | The current sign carries little duration evidence | 24h range and flip count |

| Extreme negative on a thin book | Large transfer may compensate for poor capacity | Spread, depth, volume and exit cost |

Why negative on one venue can coexist with positive elsewhere

Each venue has its own participants, reference inputs, caps and update clock. The same asset can therefore show negative funding on one venue and positive funding on another. On the measured HYPE setup, Bluefin was negative while Extended was positive, creating a large cross-venue difference.

Before comparing, normalize the interval. The BTC comparison shows 1-hour, 4-hour and 8-hour prints side by side; their raw percentages are not directly comparable.

How to read a negative funding print

- Confirm the sign convention and which side receives on that venue.

- Verify the interval and normalize only after it is proven.

- Convert the rate into dollars at the intended notional.

- Calculate the round-trip break-even hours.

- Compare break-even with 24-hour persistence: range, flips and same-sign duration.

- Measure spread and book depth at the intended size.

- Compare open interest, volume, freshness and venue health.

PerpRadar keeps those fields together on the cross-venue funding view, so the minus sign never appears without its interval and market context.

FAQ

- What does a negative funding rate mean?

- It means SHORT legs pay LONG legs for that venue and funding interval. The direction is the reverse of positive funding.

- Does negative funding mean the price will rise?

- No. It can indicate a perp discount or crowded short exposure, but those conditions can persist while price continues lower. Funding is not a reversal timer.

- Can the same asset have positive and negative funding?

- Yes. Different venues have different participants, reference inputs and update clocks. One venue can print negative funding while another is positive for the same asset.

- Why should I check the funding interval?

- Because −0.01% per hour is very different from −0.01% per eight hours. Normalize only after confirming each venue’s actual interval.

- How do I estimate negative-funding break-even time?

- Divide the total round-trip cost percentage by the absolute hourly funding percentage. Then compare the required hours with recent same-sign duration and flip history.